हिंदी में पढ़ने के लिए मेनू बार से हिंदी भाषा चयन करें।

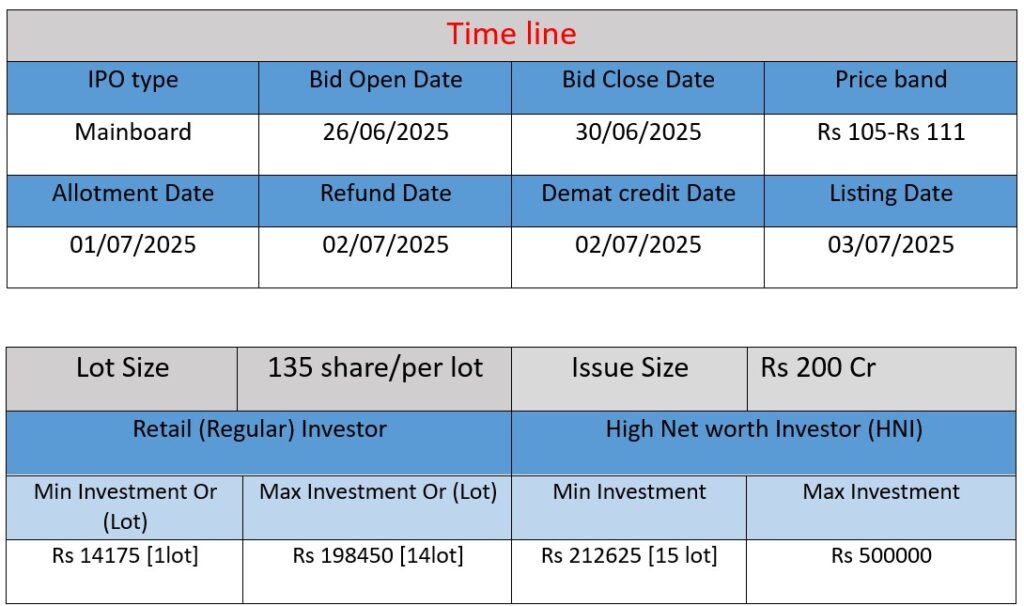

Indogulf Cropsciences IPO opens with an issue size of ₹200 crore, aiming to fund working capital needs, repay debt, and expand manufacturing capacity. With over 400 agrochemical products and a strong export presence in 34+ countries, the company targets growth through innovation and global outreach. Stay updated on IPO dates, price band, and listing details.

Core Business

- Founded in 1993 as Jai Shree Rasayan Udyog Ltd, renamed Indogulf Cropsciences in 2015.

- Three main verticals:

- Crop protection – insecticides, herbicides, fungicides, plant growth regulators in advanced formulations like WDG, SC, CS, ULV.

- Plant nutrients – micronutrient fertilizers and deficiency correctors.

- Biologicals – bio-stimulants such as seaweed, humate, mycorrhiza.

- Backward integration: indigenous production of high-purity SPIROMESIFEN and PYRAZOSULFURON technicals (96.5% & 97%).

Strengths

- Established track record: Over 30 years in agrochemical manufacturing.

- Robust R&D & product portfolio: Over 400 products, multiple advanced formulations, with patented processes and growing registrations across 17+ countries.

- Quality credentials: ISO 9001 & 14001, NABL‑accredited labs, “Two‑Star Export House” status.

- Strong distribution: Network of ~6,900+ distributors, 192 institutional partners in India, and 143 overseas partners; presence in 22 states + 3 UTs & 34+ export markets.

- Global reach: Exports to 34+ countries with subsidiaries in Australia and India.

- Financial traction: FY24 revenue ~₹552 Cr, net profit ₹28 Cr (≈26% YoY growth), EBITDA margin at ~10.8%.

Risks & Challenges

- Agro-climatic dependency: Demand tied to monsoons and weather conditions; vulnerable to seasonal variation .

- Raw material volatility: 25–30% of inputs imported; subject to forex fluctuations, global supply disruptions.

- Regulatory & competitive risks: Agrochemical approvals vary globally; faces intense competition from domestic and multinational firms.

- Capital & execution risk: Heavy working capital needs; ongoing dry‑flowable plant project in Sonipat adds exposure to cost overruns and execution delays.

- Environmental & market transitions: Growing global preference for organic farming may dent chemical-based demand; also regulatory pressures on environment and compliance.

Conclusion

Indogulf Cropsciences is a well-established, R&D-driven agrochemical firm with a diversified product portfolio, strong export credentials, and solid financials. Its advanced technical capabilities and wide distribution network bolster its competitiveness. However, it operates in a volatile sector marked by climatic dependency, raw material exposure, regulatory unpredictability, and an evolving shift toward organic farming. Investors should consider these risks alongside the company’s strengths and the potential upside from its upcoming IPO (₹200 Cr), aimed at bolstering working capital, reducing debt, and expanding plant capacity. Consensus from market analysts is generally positive, citing structural advantages but urging caution around sector-specific risks